Some BCCs indicated by entrepreneurs when transferring taxes and insurance contributions are the same for all individual entrepreneurs, regardless of the applied taxation regime. But some budget classification codes are “intended” for a specific regime.

KBK: IP contributions 2019

BCCs for insurance premiums represent the largest group of codes that are necessary for entrepreneurs of absolutely all taxation regimes.

Individual entrepreneurs, when filling out payments for insurance premiums in 2019, must indicate the following BCC:

| Type of contribution | KBK |

|---|---|

| Insurance premiums for OPS | 182 1 02 02010 06 1010 160 |

| Insurance premiums for compulsory medical insurance | 182 1 02 02101 08 1013 160 |

| Insurance premiums for VNiM | 182 1 02 02090 07 1010 160 |

| Insurance premiums for injuries | 393 1 02 02050 07 1000 160 |

| Additional insurance contributions to compulsory pension insurance for employees who work in conditions that give the right to early retirement, including: | |

| 182 1 02 02131 06 1010 160 | |

| - for those employed in jobs with hazardous working conditions (clause 1, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ | 182 1 02 02131 06 1020 160 |

| ) (additional tariff does not depend on the results of the special assessment) | 182 1 02 02132 06 1010 160 |

| - for those employed in jobs with difficult working conditions (clauses 2-18, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (additional tariff depends on the results of the special assessment) | 182 1 02 02132 06 1020 160 |

KBK: individual entrepreneur contributions for himself

The BCC for individual entrepreneurs' contributions for themselves is also the same for everyone, regardless of the regime applied.

KBK for individual entrepreneurs on OSN in 2019

General-regime entrepreneurs are payers of personal income tax in relation to their income and payers of VAT:

KBK for individual entrepreneurs in special modes in 2019

For each special regime tax, its own BCC has been approved.

KBC penalties for personal income tax 2019-2020 are important for every accountant to know. In case of delay in making a tax payment to the budget, it is still necessary to transfer tax penalties. For this you need to use the correct KBK.

Procedure for paying personal income tax

Currently, personal income tax is charged on income taxed at a rate of 13%, in accordance with clause 3 of Art. 226 of the Tax Code of the Russian Federation, occurs on the date of receipt of income, and its transfer to the budget is no later than the next day after payment (clause 6 of Article 226 of the Tax Code of the Russian Federation).

Read more about the procedure for paying personal income tax in the article “The procedure for calculating and the deadline for transferring income tax from wages in 2019” .

If the income paid is vacation amounts or sick leave benefits, personal income tax can be transferred on the last day of the month of payment (clause 6 of Article 226 of the Tax Code of the Russian Federation).

For information on paying personal income tax on vacation pay, see.

According to Art. 223 of the Tax Code of the Russian Federation, income for the purpose of calculating personal income tax arises, as a rule, at the time of its receipt. However, there are other situations: when approving an employee’s advance report, when issuing borrowed funds to him with savings on interest, income is considered received on the last day of the month (subclause 6-7, clause 1, article 223 of the Tax Code of the Russian Federation).

Read about personal income tax on travel expenses.

Personal income tax reporting

Tax agents now have to report on personal income tax not only annually, but also quarterly. Quarterly reporting (form 6-NDFL) applies only to employers. It must be submitted based on the results of reporting periods, determined quarterly on an accrual basis, on the last day of the month following the next period. The reporting contains general tax information for all employees as a whole.

Find a selection of materials on filling out the 6-NDFL calculation in our website of the same name section .

At the same time, the annual obligation for employers to submit certificates about employees 2-NDFL, and individual entrepreneurs and (in certain situations) individuals declarations in form 3-NDFL is retained.

Read about the features of preparing 2-NDFL certificates in the material “The nuances of filling out form 2-NDFL in 2019”.

KBC on penalties for personal income tax in 2019-2020

Late submission of reports in accordance with clause 1.2 of Art. 126 of the Tax Code of the Russian Federation is fraught for the employer with a fine of 1000 rubles. for each month (for form 6-NDFL), 200 rubles. for each 2-NDFL certificate. Transfer of incorrect information, in accordance with paragraph 1 of Art. 126.1 of the Tax Code of the Russian Federation will entail liability in the amount of 500 rubles. for each incorrectly completed report.

But in case of late payment of personal income tax, you will have to not only pay off the debt, but also pay penalties. The BCC for the transfer of fines remained the same:

- 182 1 01 02010 01 2100 110 - penalties for personal income tax transferred by tax agents.

- 182 1 01 02020 01 2100 110 - penalties for personal income tax for individual entrepreneurs, lawyers, notaries.

- 182 1 01 02030 01 2100 110 - penalties for personal income tax for individuals who received income listed in Art. 228 Tax Code of the Russian Federation.

- 182 1 01 02040 01 2100 110 - penalties for personal income tax for non-residents on payments made in accordance with Art. 227.1 Tax Code of the Russian Federation.

Calculatet amountPeny nabout personal income tax is possible using our auxiliary service

How do personal income taxes apply to employees in 2017? Have the new BCCs for income tax been approved? You will find a table with a breakdown of the current BCCs for personal income tax for 2017, as well as a sample payment order for personal income tax for 2017 in this article.

When to pay tax

General approach

As a general rule, in 2017 personal income tax must be paid no later than the day following the day the employee (individual) was paid income. So, let’s say the employer paid the salary for January 2017 on February 9, 2017. The date of receipt of income will be January 31, 2017, the date of tax withholding will be February 9, 2017. The date no later than which personal income tax must be paid to the budget, in our example – February 11, 2017.

Benefits and vacation pay

Personal income tax withheld from temporary disability benefits, benefits for caring for a sick child, as well as from vacation pay must be transferred no later than the last day of the month in which the income was paid. For example, an employee goes on vacation from March 6 to March 23, 2017. Vacation pay was paid to him on March 1. In this case, the date of receipt of income and the date of withholding personal income tax is March 1, and the last date when personal income tax must be transferred to the budget is March 31, 2017.

In general, pay the withheld personal income tax in 2017 to the details of the Federal Tax Service with which the organization is registered (paragraph 1, clause 7, article 226 of the Tax Code of the Russian Federation). Individual entrepreneurs, in turn, pay personal income tax to the inspectorate at their place of residence. However, individual entrepreneurs conducting business on UTII or the patent taxation system transfer tax to the inspectorate at the place of registration in connection with the conduct of such activities.

However, the BCC for personal income tax for employees in 2017 did not change and remained exactly the same. The BCC on personal income tax for individual entrepreneurs has not undergone any amendments. We present in the table the current main BCCs for 2017 for income tax.

Sample payment order 2017

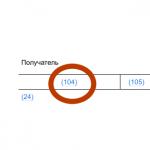

The budget classification code (BCC) must be indicated in field 104 of the payment order for the payment of personal income tax.

The general rule is: the tax agent organization is obliged to transfer income tax for employees within 1 day from the day the wages were issued. It turns out that if your company issued wages for December 2016 on January 9, 2017, you need to pay the tax no later than 01/11/17. In this example, the date of accrual of income is 12/31/16, the date of receipt of income is 01/09/17 ., the deadline for personal income tax payment is strictly until January 11, 2017.

The BCC of personal income tax for 2017 can be presented in the following table:

Before you pay, you need to understand how to calculate your income taxes. Let's look at the situation using the following practical example:

- a mandatory federal tax, it was introduced by the Tax Code of the country. The deduction is made from the wages of all employees of the enterprise by the employer, who in this case acts as a tax agent for personal income tax. 13% is withheld from the remuneration of both “full-time employees” at the main place of work, and part-time workers, and citizens providing professional services on the basis of contract agreements. The following formula is used for calculation:

Income tax = Base * Rate / 100

The tax base is the amount of remuneration reduced by deductions. The rate depends on the type of taxable income, for example:

- 13% is collected from employee salaries as a base amount. It applies to income received as part of the work activities of all residents of the Russian Federation. A similar tax rate is established for income from the use of own property as an object of rent or sale.

- The 35% tax will be on income that the taxpayer received in the form of prizes and winnings in the part that exceeds the limit established by law. The same tax rate applies to income in the form of bank interest if its value exceeds the limit determined by law. Withholding at a rate of 35 will also be applied to savings on interest on loans.

- 30% - this is how much must be withheld from the income of enterprise employees who do not have tax resident status in the Russian Federation. For them, the basic salary rate of 13% is not valid. Their income is taxed at higher interest rates. A different amount of deductions will be if a non-resident receives dividends from participation in an organization in the Russian Federation.

- 15% will have to be paid by a non-resident who took part in the activities of a Russian organization and received dividends. It turns out that if you are not a tax resident of the Russian Federation and at the same time receive income as the owner of a Russian company, from this amount you are required to pay 15% to the country's budget.

- 9% will be paid to the budget by Russian resident founders, who were paid dividends based on the results of the company’s work. At a similar rate, income that was received by the taxpayer as interest on bonds that are mortgage-backed and issued before January 1, 2007 is taxed.

For example, Svetlana Vasilyeva in 2016 received a salary of 1,250,845 rubles. (the amount is indicated in full, before tax withholding), excess interest on the placed loan in the amount of RUB 170,000. and dividends from participation in Svetelka LLC in the amount of RUB 500,000. (amount is indicated before income tax).

She must pay personal income tax in the following amount:

- 13% from salary – 1,250,845 * 13% = 162,610 rubles.

- 35% from excess interest – 170,000 * 35% = 59,500 rubles.

- 9% on dividends as a resident – 500,000 * 9% = 45,000 rubles.

Svetlana Vasilievna’s total personal income tax for 2016 will be 267,110 rubles.

Now you need to list them correctly, and to do this, familiarize yourself with the current personal income tax codes in force in 2017.

KBK NDFL 2017

If you carefully read the revisions of the laws, it turns out that the KBK personal income tax 2017 for employees remained the same. Usually, at the end of the tax period at the very beginning of the next year, the Ministry of Finance notifies in letter format about how personal income tax payments to KBC 2016 will look like in the new year. The latest document on this issue is dated 07/01/13 and has No. 65n. It is still relevant now, which means that new personal income tax tax codes for 2017 have not been established and you can send taxes with the old details and this will not be a violation. Look in the table below to determine which personal income tax tax code to set for employees in 2016:

Let's look below at various situations when taxes are transferred by an individual entrepreneur or LLC, in addition, you need to pay penalties and make payments on income taxed at different rates.

KBK NDFL 2017 for LLC employees

The code that must be indicated in the payment slip when transferring personal income tax for employees has not changed, and it is the same for JSC and LLC in 2016-2017. and has the form 182 1 01 02010 01 1000 110. By the way, the transfer of personal income tax in 2016 to the KBK is carried out according to the rules that are in force in 2015. The payment order will look like this:

Using this form, you will need to pay tax for employees from their March 2017 salary.

KBK NDFL 2017 for employees for individual entrepreneurs

It is necessary to distinguish between the code for transferring tax for the entrepreneur himself and the KBK Personal Income Tax 2016 for individuals who are his employees. In the first case, you need to enter KBK 182 1 01 02020 01 1000 110 - this is for individual entrepreneurs who pay tax on their activities, in the second, the code will be similar to KBK Personal Income Tax Agent 2016.

KBC penalties for personal income tax 2017

The country's tax authorities may assess penalties if the tax agent does not timely remit taxes on the income of its employees. By the way, penalties are not always collected legally; in some cases, the organization may well cancel them.

It is necessary to clarify the KBK personal income tax penalty if you actually have a debt under the KBK to pay personal income tax for 2016. In this case, it will need to be repaid as quickly as possible and penalties accrued by the department must be paid.

If you paid personal income tax, but sent it according to the correct KBK for transferring personal income tax in 2016, but all to the head office, this should not be a reason for charging you penalties, because the violation affected the payment procedure, for which there are no penalties.

This position is reflected in regulated acts. For example, it was disclosed in letter BS-4-44/5717 of the Federal Tax Service dated 04/07/15 and confirmed by judicial practice in Resolution 14519/08 of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 03/24/09.

If money was withdrawn from you using the code KBK NDFL 2016 with the purpose of payment “Peny”, and you think that this is illegal, write a request for a refund. If there is no understanding on the part of the territorial Federal Tax Service, leave a complaint to a higher authority.

Penalties for personal income tax may also be charged on unwithheld tax. The KBK income tax for 2017 did not change, and for this position there may be a shortage of transfers from which the inspector will try to collect penalties.

In this case, there is already an official position of the department, namely the letter of the Federal Tax Service ED 4 2/13600 dated 08/04/15, according to which the tax office does not have the right to charge penalties on KBC for the payment of personal income tax in 2017 from the amount that the agent could not withhold.

KBK dividends in 2017 personal income tax

Let's take a separate look at the rules for calculating and paying income tax on dividends and the specific procedures for residents and non-residents of the country. practice shows that not many enterprises pay dividends, much more often the founder is brought into the staff and paid his salary, but there are no funds or sources left for dividends. However, if you have to make such a payment to KBK NDFL dividends 2017, be prepared to fill out a payment order. It will look something like this:

182 1 01 02010 01 1000 110 – KBK personal income tax on dividends, rate 13% for residents and 15% for non-residents of the country. Non-residents who have stayed in Russia for more than 183 days while having a residence permit will also pay tax at a reduced rate.

KBK personal income tax for material benefits 2016

First, you need to figure out when, from whom and under what circumstances taxable income in the form of material benefit may arise. To do this, you will need to carefully study the current tax legislation. The main cases are already known when an employee has a personal income tax KBK in 2017 for material benefits:

- In the current tax period, the taxpayer managed to save on interest when using credit funds

This excess is recorded taking into account the following rules: 2/3 of the key rate in comparison with the taxpayer’s interest approved by the current agreement

- The taxpayer received material benefits from transactions with securities and financial instruments

Here we calculate the amount of excess of the price of a security over the actual expenses of a given taxpayer

- The taxpayer enriched himself during procurement through transactions between related parties

The price of the analogue, which is sold on the real market, is used as a standard for comparison.

Taxation benefits will not arise in the following cases:

- there is a benefit, but it was formed due to the special grace period for using a credit card

- there is a benefit, but it is due to savings on interest on borrowed funds that the taxpayer raised for the purchase or construction of housing

A taxpayer may be exempt from income tax on material benefits if it is prescribed to him on the basis of the provisions of Article 220 of the Tax Code of the Russian Federation.

If you find an error, please highlight a piece of text and click Ctrl+Enter.